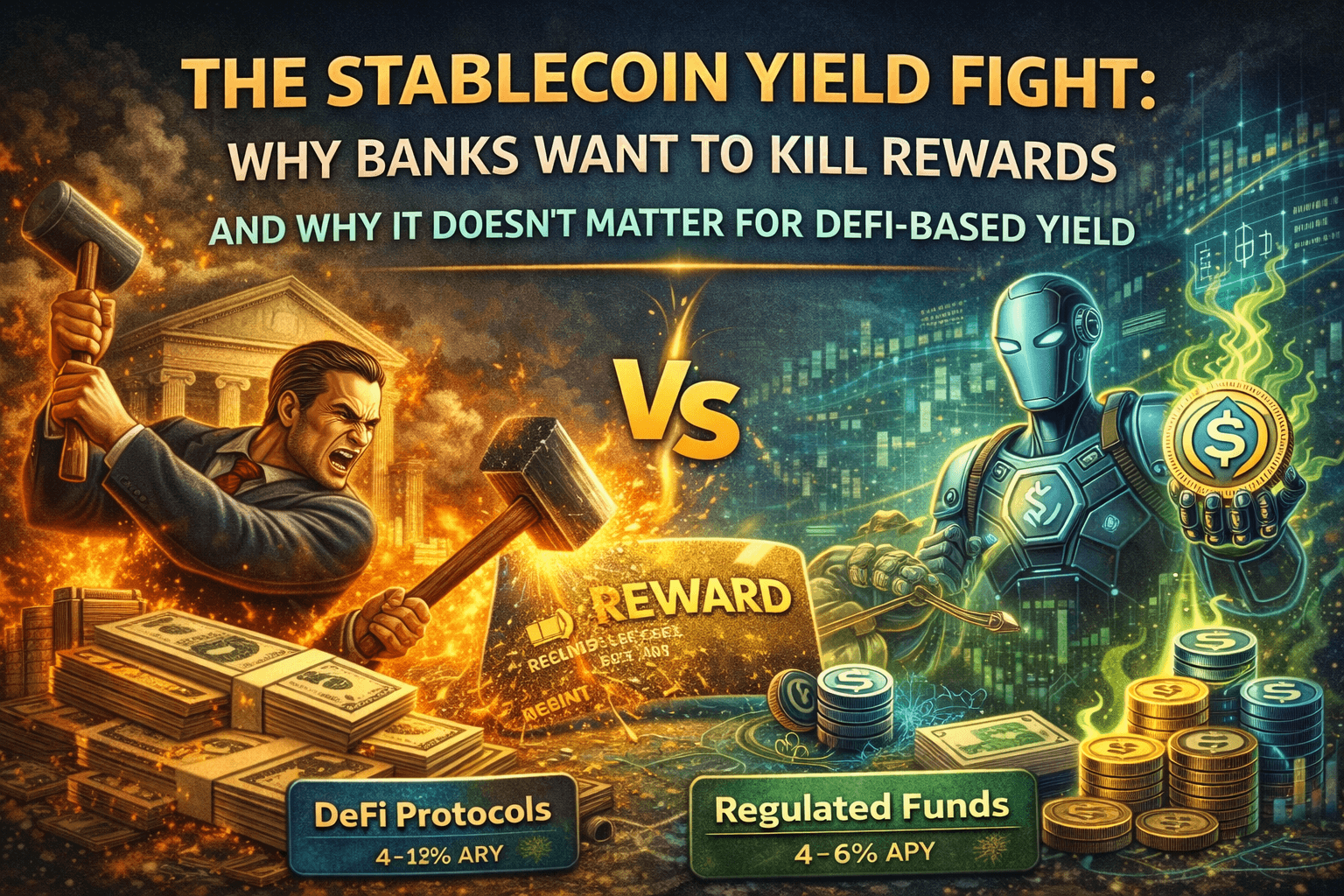

The fight over stablecoin yield is not about yield. It's about who controls the funding advantage that yield creates.

Circle pays Coinbase a share of the interest earned on USDC reserves. Coinbase passes some of that to users as "rewards." Banks call this a loophole. Coinbase calls it competition. Congress is caught in the middle. And the entire debate misses a fundamental point: yield from lending protocols operates on completely different infrastructure.

If your stablecoin yield comes from DeFi lending markets rather than issuer revenue sharing, this fight does not apply to you.

What Is the Stablecoin Yield Loophole?

The GENIUS Act, signed July 2025, prohibits stablecoin issuers from paying interest or yield directly to holders. Circle cannot pay you for holding USDC. PayPal cannot pay you for holding PYUSD.

But the law says nothing about third parties.

Circle earns interest on the Treasury bills backing USDC reserves. Through revenue-sharing agreements, Circle pays Coinbase for distribution and customer acquisition. Coinbase then offers users 4.1% APY as "USDC Rewards." PayPal runs the same playbook with PYUSD at 3.7%.

Coinbase CEO Brian Armstrong's position: "We are not the issuer. We don't pay interest or yield. We pay rewards."

Banks see it differently. The Bank Policy Institute told Congress in August 2025 that this structure "undermines" the GENIUS Act's intent and could trigger $6.6 trillion in deposit outflows from traditional banks.

Why Did Coinbase Pull Support for the CLARITY Act?

The CLARITY Act was supposed to establish broader crypto market structure rules. Then banking lobbyists pushed amendments to close the rewards loophole.

On January 14, 2026, Armstrong announced Coinbase would not support the bill. "We'd rather have no bill than a bad bill," he wrote. The Senate Banking Committee postponed its markup vote indefinitely.

The stakes are material. Coinbase reported $355 million in stablecoin revenue in Q3 2025, nearly 20% of total revenue. The company says rewards drive USDC growth on its platform. Killing rewards kills the growth engine.

Armstrong at Davos: "Banks should have to play on a level playing field. If stablecoin rewards can offer Americans more, maybe banks should pay higher interest rates to compete."

The banking lobby disagrees. They argue yield-bearing stablecoins function like deposits and should face the same regulatory burden.

What Happens If the Loophole Closes?

If Congress extends the yield prohibition to affiliates and distributors, the Circle-Coinbase model breaks.

Coinbase could no longer offer USDC rewards funded by Circle's reserve income. PayPal could no longer offer PYUSD yields. Any platform receiving issuer revenue sharing and passing it to users would face restrictions.

The current negotiation centers on whether "loyalty programs" and "promotional rewards" get carved out or whether the prohibition covers any economic benefit flowing from issuer reserves to end users.

Banks want the broadest possible definition. Crypto platforms want the narrowest.

Why DeFi-Based Yield Is Different

The entire debate assumes yield flows from issuer reserves through revenue-sharing agreements to platforms to users. That is one model. It is not the only model.

Yield from DeFi lending protocols has a completely different source.

When stablecoins are deposited into a lending protocol like Drift, Aave, or Morpho, they are lent to borrowers who pay interest. The yield comes from borrower demand, not from issuer reserves. There is no revenue-sharing agreement with Circle or any stablecoin issuer.

This distinction matters legally. The GENIUS Act and proposed CLARITY Act amendments target the relationship between issuers and the parties distributing their stablecoins. DeFi protocols are not distributors. They are neutral infrastructure that anyone can use.

How Infrastructure Providers Access DeFi Yield

Companies like RebelFi build infrastructure that enables businesses to access DeFi yield on their stablecoin holdings without managing protocol complexity directly.

The architecture: a fintech or payment company holds stablecoins in treasury or operational float. RebelFi's infrastructure deploys those stablecoins to vetted lending protocols. Yield accrues from borrower interest payments. The company earns returns on capital that would otherwise sit idle.

This is not issuer revenue sharing. This is capital deployment into lending markets, the same fundamental activity that banks perform when they lend deposits.

The yield source is borrower demand on Drift or similar protocols, currently 6-9% APY on stablecoin deposits. No Circle revenue share. No PayPal partnership agreement. No issuer relationship at all.

Does the Loophole Debate Affect DeFi Yield?

No. The loophole debate is specifically about:

Whether stablecoin issuers can indirectly pay yield through affiliated platforms

Whether "rewards" funded by issuer reserve income violate the GENIUS Act prohibition

Whether Congress should extend the ban to distributors and affiliates

DeFi lending protocols do not receive payments from stablecoin issuers. They do not have revenue-sharing agreements. They are not distributors or affiliates. They are permissionless smart contracts that match lenders with borrowers.

Infrastructure providers accessing these protocols are not in the distribution chain that the loophole debate targets. They are deploying capital into lending markets, an activity with centuries of legal precedent.

What Fintechs Should Understand

If your yield strategy depends on issuer revenue sharing, you are exposed to regulatory risk. The CLARITY Act debate may or may not resolve in your favor, but the uncertainty itself creates business risk.

If your yield strategy depends on DeFi lending protocols, you are not party to this debate. Your yield comes from a fundamentally different source with a fundamentally different legal structure.

The practical implication: infrastructure that accesses lending protocol yield provides a more durable path to stablecoin returns than infrastructure dependent on issuer relationships.

The Bigger Picture

The stablecoin yield fight is really a fight over who captures the funding advantage that stablecoins create.

Banks want stablecoins to function purely as payment instruments with no yield component. That preserves their deposit franchise.

Crypto platforms want to offer yield because it drives adoption and creates sticky user relationships.

DeFi protocols are neutral infrastructure that enables anyone to earn lending yields regardless of how this political fight resolves.

For businesses holding stablecoins operationally, the question is which yield infrastructure you build on. Infrastructure tied to issuer revenue sharing faces regulatory uncertainty. Infrastructure tied to lending protocols does not.