Every payment company has a hidden asset: settlement buffers. These are the stablecoins held between receiving deposits and disbursing payouts, the reserves maintained for settlement guarantees, and capital staged for anticipated outflows. Most treat these funds as dead weight earning nothing.

A mid-sized processor holding $10 million in average buffer is leaving $600,000-$900,000 annually on the table. This guide explains how to transform idle settlement capital into revenue while maintaining instant liquidity.

What Settlement Buffers Actually Cost You

Settlement buffers exist across several operational categories that most payment companies never optimize.

Pre-settlement float covers customer deposits awaiting settlement completion, typically spanning 1-5 days depending on the payment rails involved. These funds sit in operational wallets, fully liquid and ready for disbursement, but generating zero returns.

Operational reserves include capital maintained for settlement guarantees, regulatory requirements, and working capital needs. Payment service providers often hold 10-20% above minimum requirements as a safety margin, creating substantial pools of unproductive capital.

Escrow holdings accumulate in marketplaces and platforms holding funds between buyers and sellers during fulfillment periods, dispute windows, or verification processes. These can represent significant capital depending on transaction volumes and hold periods.

FX timing buffers are stablecoins held for optimal conversion timing in multi-currency operations. Companies processing cross-border payments frequently maintain positions across several stablecoin denominations.

The common thread: traditional payment infrastructure leaves all this capital completely unproductive. Operational float doesn't sit in interest-bearing accounts. It sits in hot wallets and operational checking accounts earning 0%.

Here's the real cost for a processor with $10 million average buffer:

Scenario | Annual Yield | Revenue Impact |

Current reality (0% operational float) | $0 | Baseline |

Conservative DeFi (6% APY) | $600,000 | +$600,000 |

Optimized Strategy (8% APY) | $800,000 | +$800,000 |

That's not a marginal improvement. It's pure new revenue that compounds every year your competitors capture it and you don't.

Where Yield Comes From in 2026

The stablecoin market exceeded $308 billion by December 2025, with USDT commanding approximately 60% at $186 billion and USDC holding 25% at $78 billion. More importantly, yield infrastructure has professionalized with options for every risk profile.

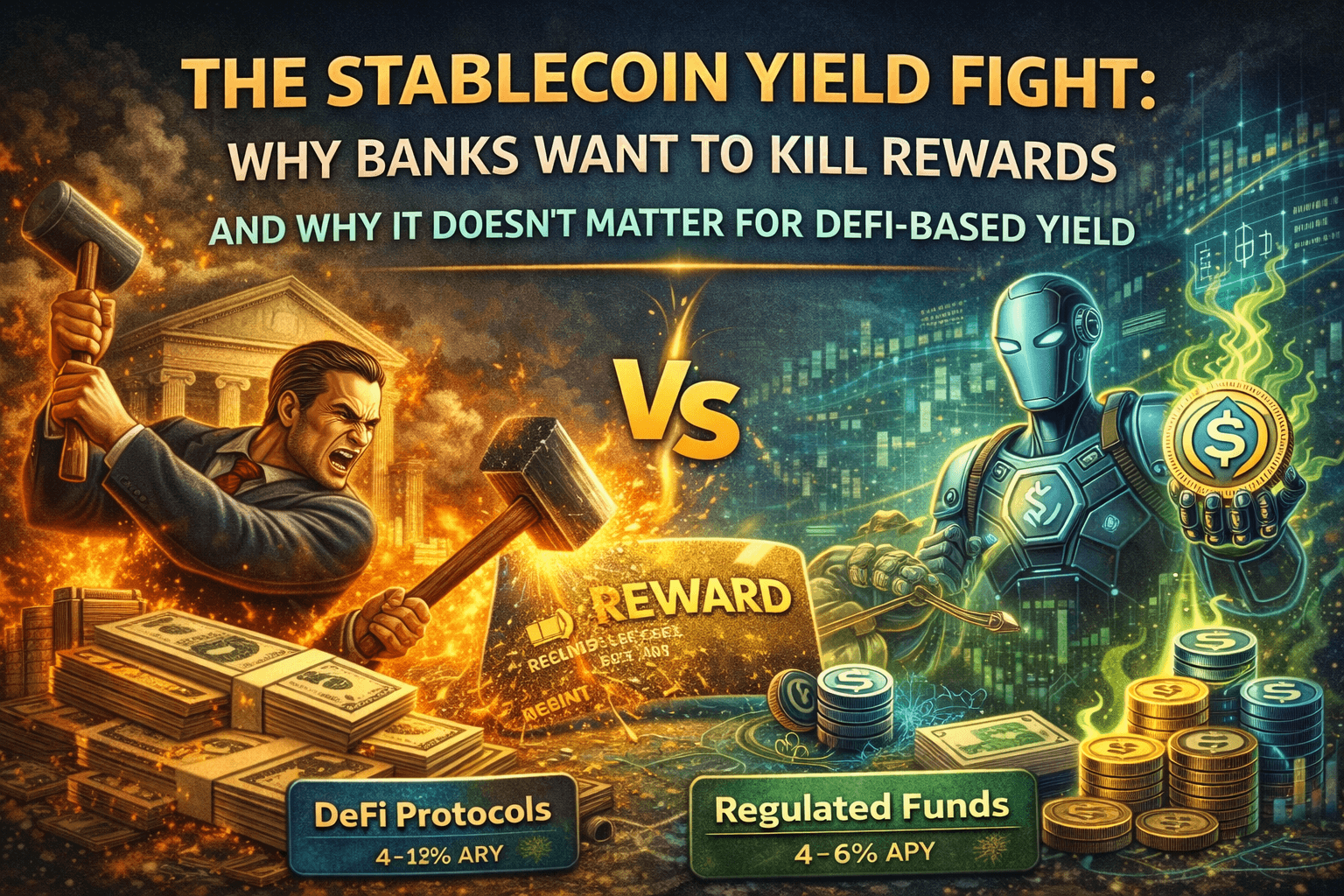

DeFi lending protocols offer the highest yields, typically 5-12% APY depending on market conditions. Aave V3 provides 4-7% on USDC with institutional-grade security and liquidity pools exceeding $825 million in TVL. Drift Protocol on Solana delivers 6-9% APY with single-transaction deposit and withdrawal flows.

Tokenized treasury products provide regulated middle ground between traditional finance and DeFi. Franklin Templeton's BENJI fund has expanded across multiple blockchains with over $580 million in assets, offering 4-5% APY backed by short-term U.S. Treasury securities. BlackRock's BUIDL fund, launched in partnership with Goldman Sachs and BNY Mellon, enables blockchain-recorded money market fund ownership with similar yields.

Stablecoin-specific lending through protocols like Venus Protocol yields 4-5% APY with lower gas costs on BSC networks, while Compound provides comparable rates on established Ethereum infrastructure.

The critical factor for payment operations: modern DeFi protocols now offer same-block liquidity. Funds deployed to yield can be withdrawn in seconds, not days, making yield generation fully compatible with operational requirements for instant access.

How Programmable Yield Works

The mechanics of earning yield on settlement buffers have simplified dramatically. Here's the process in practice:

When funds arrive in your operational wallet, smart contract infrastructure can automatically route them to yield-generating protocols. This happens atomically, meaning deployment occurs in the same blockchain transaction as the deposit, with no manual intervention required.

While funds sit in yield protocols, they continue earning continuously. At current rates, $1 million in settlement buffer generates approximately $55-75 daily at 6-9% APY. For a payment processor maintaining $10 million in average buffer, that translates to $550-750 daily or $200,000-275,000 annually.

When disbursement is needed, withdrawal transactions execute in under 30 seconds on Solana-based protocols. Funds return to your operational wallet with full liquidity, ready for immediate payout.

The yield compounds continuously. Unlike traditional finance where interest accrues monthly or quarterly, DeFi protocols calculate yield per block, meaning every minute your funds sit deployed adds to returns.

The GENIUS Act Makes This Compliant

The regulatory environment now explicitly supports this model. The GENIUS Act, signed into law on July 18, 2025, prohibits stablecoin issuers from paying interest or yield directly to holders. However, the legislation does not prevent third-party infrastructure providers from offering yield services.

This creates clear legal separation: stablecoin issuers like Circle (USDC) and Tether (USDT) cannot pay you yield for holding their tokens, but infrastructure providers can help you deploy those tokens into yield-generating protocols.

Major law firms including Latham & Watkins and Sidley Austin have confirmed this interpretation. The prohibition applies specifically to payments "in connection with the holding, use, or retention" of stablecoins by issuers. Third-party DeFi protocols and infrastructure providers fall outside this restriction.

The distinction matters for compliance. Payment companies working with third-party yield infrastructure operate within established regulatory boundaries while capturing returns that issuers themselves cannot provide.

Implementation Framework

Successful implementation requires matching yield strategy to operational requirements. Payment companies should consider a tiered approach:

Tier 1 (Immediate access, 10-20% of buffer): Maintain in hot wallets for real-time processing with zero yield. This ensures transaction speed never suffers.

Tier 2 (Same-block access, 60-70% of buffer): Deploy to high-liquidity protocols on Solana or Ethereum L2s where withdrawals settle in seconds. Target 6-8% APY through established lending protocols.

Tier 3 (Same-day access, 10-20% of buffer): Allocate to tokenized treasury products for regulated yield at 4-5% APY. These instruments require slightly longer withdrawal windows but carry lower smart contract risk.

Allocation percentages should reflect your specific operational patterns. A payment processor with highly predictable weekly disbursements can deploy more aggressively to Tier 2 and Tier 3. Platforms with volatile, real-time payout requirements should maintain larger Tier 1 allocations.

Custody and Compliance Architecture

Payment companies managing customer funds face additional compliance requirements. The solution involves wallet ring-fencing, an architecture used by major institutions including Coinbase, Fireblocks clients, and regulated exchanges.

Core principle: Customer funds never flow directly into DeFi protocols. Instead, separate wallet layers create compliance-safe boundaries.

Customer deposit wallets receive inbound payments and undergo KYT screening. These wallets never interact with DeFi.

Operational wallets consolidate balances and prepare funds for disbursement or yield deployment. A second KYT gate ensures only clean funds proceed.

Treasury wallets hold institution-owned capital eligible for DeFi interaction. These receive funds only from verified internal sources, never directly from external deposits.

DeFi interaction wallets maintain protocol-specific positions. They connect only to treasury wallets and pre-approved protocols.

This architecture ensures compliance with AML requirements while enabling yield generation on operational reserves and company-owned capital.

Calculate Your Opportunity

A straightforward formula estimates annual yield potential:

Average settlement buffer × yield rate × deployment percentage = annual revenue

Practical calculation steps:

Calculate average daily stablecoin balance across all operational wallets over the past 90 days

Identify what percentage represents company-owned capital versus customer funds in transit

Estimate realistic deployment percentage based on your disbursement velocity

Apply conservative yield assumptions (6% rather than peak rates)

Example for a mid-sized payment processor:

Average daily buffer: $8 million

Company-owned portion eligible for full deployment: $3 million

Customer transit funds with 70% deployable: $5 million × 70% = $3.5 million

Total deployable: $6.5 million

Conservative yield at 6% APY:

$390,000 annually

Actual implementation typically recovers 60-80% of theoretical maximum due to practical constraints around deployment timing and liquidity requirements. Even at 60% capture rate, this example generates $234,000 in new annual revenue.

Risk Management

Yield generation involves risks that payment companies must manage explicitly.

Smart contract risk represents the possibility that protocol code contains vulnerabilities. Mitigation strategies include limiting exposure to any single protocol to 30-40% of deployed capital, using only protocols with multiple third-party audits, and maintaining insurance coverage through providers like Nexus Mutual (2-4% annual cost).

Protocol liquidity risk emerges when withdrawal demand exceeds available liquidity. Selection criteria should prioritize protocols with TVL exceeding $100 million and consistent utilization rates below 90%.

Yield volatility means returns fluctuate based on market demand for borrowing. Building strategies around conservative yield assumptions (4-5% rather than advertised rates) creates margin for rate compression.

For payment companies managing customer capital, smart contract insurance often represents prudent risk management rather than optional expense.

Build vs. Buy Decision

Payment companies face a strategic choice: build yield infrastructure in-house or partner with specialized providers.

Building in-house requires blockchain engineering expertise, ongoing protocol monitoring, smart contract security practices, and compliance infrastructure. Development costs typically range from $500,000 to $2 million with 12-18 month timelines before deployment.

Managed infrastructure through providers like RebelFi offers custody-agnostic yield optimization where payment companies maintain control through existing custody solutions (Fireblocks, BitGo, Tatum) while accessing institutional DeFi yields. Integration timelines compress to days rather than months, and providers handle protocol selection, rebalancing, and risk monitoring.

The economics favor managed solutions for most payment companies. Even with provider fees (typically 20-40% of generated yield), net returns significantly exceed traditional banking while avoiding substantial development investment.

The Competitive Window

Payment companies implementing yield strategies today establish advantages that compound over time. A competitor earning 6% on $10 million in settlement buffers generates $600,000 annually that funds better customer terms, absorbs fee compression, or drops directly to margin.

Visa's December 2025 launch of stablecoin settlement for U.S. banks demonstrates institutional adoption has moved from pilot to production. As stablecoin adoption accelerates, capital held in settlement buffers will only grow.

The infrastructure exists. Regulatory frameworks support deployment. For payment companies holding significant stablecoin balances, the question has shifted from whether to pursue yield on settlement buffers to how quickly you can implement a strategy that transforms idle operational capital into sustainable revenue.

RebelFi builds programmable stablecoin infrastructure enabling payment companies to generate yield on operational capital without custody transfer. Learn more at rebelfi.io.